National, state and local government fiscal challenges have been highlighted in the media for several years now. Since the 2008 recession, we've seen unprecedented fiscal challenges, including municipal bankruptcy, strike public institutions across the country. Local government's have attempted to address these fiscal emergencies in a variety of different ways, without much success. As the Volcker-Ravitch report recently concluded, "states and cities have deep structural problems that will not go away just because the country is coming out of the recession that started in 2008."

The Center for Priority Based Budgeting (CPBB) has been on the cutting edge in assisting local governments to navigate their way through significant fiscal challenges. As we stated in a recent CPBB article The New Wave - A Paradigm Shift in Municipal Financial Stewardship, "a key component of the paradigm shift is changing the way that resource

allocation discussions take place. Financial problems are also

effectively hidden and obscured because the budget process allows for

it. Line item budgeting, incremental budgeting, zero-based budgeting

were each attempts to better understand "how" money is spent, but these

methods fail to address a more fundamental question:"why" money is

spent."

Priority Based Budgeting (PBB) provides a scalable, replicable and comprehensive review of the entire

organization, identifying every program offered, identifying the costs

of every program offered, evaluating the relevance of every program

offered on the basis of the community's priorities, and ultimately

guiding elected and appointed officials to the policy questions they can

answer with the information gained from the Priority Based Budgeting

process, such as:

What is the local government uniquely qualified to provide, offering

the maximum benefit to citizens for the tax dollars they pay?

What is the community truly mandated to provide? What does it cost to fulfill those mandates?

What programs are most appropriate to fund by establishing or increasing user-fees?

What programs are most appropriate for establishing partnerships with other community service providers?

What services might the local government consider “getting out of the business” of providing?

Where are there apparent overlaps and redundancies in a community because several entities are providing similar services?

Where is the local government potentially competing against private businesses within its own community?

Priority Based Budgeting has now been successfully implemented in over 60 local government communities coast-to-coast. We take pride in our partnership with these CPBB communities in an effort to improve a community's fiscal health for the benefit of the entire community. The City of Boulder, Colorado recently unveiled their 2014 budget using PBB for the 4th year in a row. As the Boulder 2014 Budget Policy Document states, "Now integrated into its fourth consecutive year of budget develepmont, Priority Based Budgeting (PBB) is the framework within which all budget decisions are made."

CPBB Local Government Partners by State

The core CPBB concepts of Fiscal Health and Wellness through Priority Based Budgeting are truly inspiring a new wave of municipal fiscal stewardship. A complete revolution in how local governments utilize their limited resources to the benefit of the communities they serve. Recently, communities as economically and geographically varied as the City of Branson, Missouri, Scott County, Minnesota, the City of Hermosa Beach, California, Cobb County, Georgia and San Juan County, New Mexico have chosen priority based budgeting to fundamentally change their approach to fiscal stewardship.

This "New Wave," the fundamental paradigm shift in municipal financial stewardship, must be accepted if local governments are to be financially viable and able to create the types of communities their citizens are proud to call home.

Local government communities must consider a completely different perspective.

In order to achieve success and accept the challenges that are ahead, we

must see more clearly how to manage, use, and optimize resources in a

much different way than has been done in the past. This new environment

demands a new (economic) vision of the future.

--> Dear Members of City Council and Residents of Boulder,

I am pleased to present to

you the City Manager’s 2014 Recommended Budget for review and consideration.

This budget was developed in accordance with the City Charter, city financial

management policies and guidelines, and City Council's adopted goals. This

budget continues to recognize the national economic conditions that demand

conservative approaches to managing expenses, while providing a balance between

maintaining existing high-quality programs, services and infrastructure, and

funding enhancements and new initiatives, to best meet the priorities of the

Boulder community.

The budget is a financial

document that defines the fiscal parameters of the coming year. It is a guide

to allocation of resources in support of community goals, and it is a tool for

strategic alignment of short-and long-term financial objectives. As a part of

the process for building the 2014 Recommended Budget, city staff took a multi-year

strategic approach, as well as applying the principles of Priority Based

Budgeting. The result of this approach was a focus on strengthening core city

services and operations, such as public safety and facility maintenance, as well

as providing funding for key council initiatives and investing in the future.

City Manager, Boulder Colorado 2014 Annual Budget Message

"Now integrated into

its fourth consecutive year of budget development, Priority Based Budgeting (PBB) is the framework within

which all budget decisions are made." City of Boulder 2014 Annual Budget Policy Document

The Center for Priority Based Budgeting has proudly partnered with the City of Boulder in implementing priority based budgeting (PBB) into their annual budget process for the last four years. The City adopted priority based budgeting in 2010. During this time, the City has become a "leading practitioner" of priority based budgeting and utilizes this process in all of their short and long-term financial decisions. Read more about Boulder's success implementing PBB and their Resource Reallocation Breakthroughhere.

The City of Boulder, Colorado recently published their 2014 Annual Budget. This comprehensive policy document contains a detailed description of how the city plans to invest available resources in city operations in 2014. One of the eight main sections of the budget document is Strategy and Priorities. This section provides an in-depth look in how the city utilizes priority based budgeting for short-term and long-term budgeting and strategic economic planning. The following is an excerpt from this section.

Priority Based

Budgeting

Purpose of Priority

Based Budgeting

Priority Based

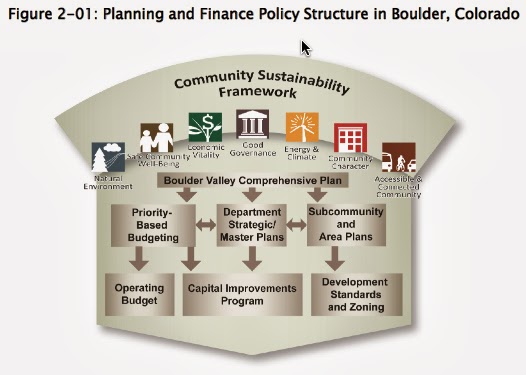

Budgeting (PBB) builds on the city’s prior Business Plan, which separates goals

and actions into near term versus long term time frames. PBB harnesses the

policies and values of the Boulder Valley Comprehensive Plan and department

strategic and master plans. As the cornerstone of the city’s budget process,

PBB gives the city three central benefits:

Identifies key

Council and community goals (see the next section on PBB Results and Attributes)

Evaluates the

impact on these goals of city programs and services

Provides a tool for

strategic decision-making in funding, adding and/or eliminating programs and

services, making more effective use of the city’s limited resources.

PBB contributes to

the city’s long-term financial sustainability and allows the city of Boulder to

serve its residents in the most effective, efficient and fiscally responsible

manner possible.

2014 Priority Based Budgeting Outcomes

Now integrated into

its fourth consecutive year of budget development, PBB is the framework within

which all budget decisions are made. In the 2014 budget process, the city was

asked to use PBB in every step of the budget process and program ranking by

quartile was included in all budget discussions throughout the year. To

maintain value and consistency in program scoring, a Peer Review Group, a

citywide team who comes together to score PBB programs and services annually,

reviewed all changes between 2013 and 2014.

The city has a

favorable distribution of resources between the highest priority (Quartile 1)

and lowest priority (Quartile 4) programs. Fewer resources are invested in

programs yielding lower impact on community values. A listing of all 2014

programs by quartile is included in the following section. Community programs

are those providing direct service to residents and businesses, while governance

programs are those providing support services within the city to other

departments.

Due to a number of

factors, including only modest revenue increase projections, with ongoing cost

increases, there was limited opportunity to add resources to city programs in

the 2014 budget. The 2014 budget process included identification of resources

for reallocation and PBB was a tool used to help shift resources from lower to

higher priority programs.

To better understand how the City of Boulder utilizes priority based budgeting as the "framework in which all budget decisions are made," click here!

Congratulations again to the City of Boulder, Colorado! You remain a

true priority based budgeting all-star and a leading PBB practitioner in

local government fiscal stewardship!

For more innovative priority based budgeting resources see links below:

"To be or not to be. That's not really a question." - Jean-Luc Godard

"States and cities have deep structural problems that will not go away

just because the country is coming out of the recession that started in

2008." - Volcker-Ravitch Report

In local government, unlike the federal government, we don't have the luxury of operating in an environment of unbalanced budgets. Cities and counties are mandated to present balanced budgets each and every fiscal year. While Godard was clearly not discussing local government finance when he stated "To be or not to be. That's not really a question," he might as well have been in this fiscal environment. For as challenging as it is for local governments to continue to present balanced budgets in the face of years of revenue shortfalls and painful service cuts, it simply must be.

The New York Times recently reported on the release of the Volcker-Ravitch report in their article Task Force Urges Local Governmens to Stop Obscuring Fiscal Troubles. The State Budget Crisis Task Force released its final report,

calling for an end to the longstanding practice of using one-offs and

opaque accounting methods that make budgets appear balanced even when

fiscal problems are worsening. "Local governments must stop using budget gimmicks that obscure the true extent of their money problems." The task force was led by a former

chairman of the Federal Reserve Board, Paul A. Volcker, and a former New

York lieutenant governor, Richard Ravitch, who have warned that states

and cities have deep structural problems that will not go away just

because the country is coming out of the recession that started in 2008.

Now, so many of us who "are in the business" of trying to balance budgets, understand and appreciate the dangers and fallacies of applying budget gimmicks. But then, why do these practices still prevail? Why do many resort to these types of solutions knowing they deny transparency, mask problems at worst, and at best, trick decision-makers into a false sense of security? Perhaps at least part of the answer is that it's difficult to conceive of any other way to solve the financial problems of the day - perhaps, for lack of another solution, budget tricks are the best solutions we have? For as fundamentally sound and true and correct as the Volcker and Ravitch report is, it's most significant achievement is pointing out where government is falling short. This begs the next question: what can be done to fix these pressing problems?

A new paradigm is required - a "New Wave" in local government Fiscal Health.

The Crisis is Not Fiscal

In part due to the recession that started in 2008, and in part to attempt a departure from the exact same types of practices outlined by Volcker and Ravitch, CPBB co-founders Chris Fabian and Jon Johnson published their first local government fiscal health and prioritization report Getting Your Priorities Straight in ICMA's PM Magazine. This paper was published prior to the existence of the Center for Priority Based Budgeting.

During this time, Jon and Chris both worked for Jefferson County, Colorado as Budget Director and Internal Business Consultant respectively. It was at Jefferson County where Jon and Chris had first started to conceive of the creative and innovative concepts of Fiscal Health and Wellness through Priority Based Budgeting.

As if predicting the New Wave, in Getting Your Priorities Straight the authors emphasize the point that the recession isn't the only driver causing local government fiscal challenges. They state, "why do local government professionals believe that this is the

crisis? What assumptions do we hold so firmly and that so calcify our

thinking to convince us that changing fiscal conditions represent our

crisis? Would higher revenues and lower expenses allow us to operate

crisis free? Or does the true crisis exist when, despite our fiscal

realities, we don’t focus on those priorities and objectives that ensure

the success of our communities?"

The authors went one step further, and just like Volcker and Ravitch, made a critical leap: the crisis facing local government is not fiscal. It's the choices we make to address the fiscal challenges. Volcker and Ravitch make the same argument when observing that the end of the recession alone will not result in better financial management.

In Reengineering the Corporation, Michael Hammer writes that

organizations suffer from “inflexibility, unresponsiveness, the absence

of customer focus, an obsession with activity rather than result,

bureaucratic paralysis, lack of innovation, and high overhead.” Why?

“If costs were high, they could be passed on to customers. If customers were dissatisfied, they had

nowhere else to turn.” Should we in government only now be concerned with flexibility,

responsiveness, customer focus, and results because we can no longer

afford not to be?

Perhaps the biggest concern we face is not a fiscal crisis. Fiscal

trends and conditions are by and large out of our control and simply

represent a reality with which we need to cope. The real crisis on our

hands is whether our organizations have the capabilities to address

current fiscal realities and still meet the objectives of government and

the expectations of our constituents.

The Imperative of "New Tools" in Creating Financial Transparency - "Data Visualization or How I Learned to Stop Worrying (and Obscuring Financial Problems) and Love Financial Transparency"

The Volcker-Ravitch report places special emphasis on the harmful impacts that budget gimmicks create when the intention is to mask or obscure financial problems. But what would true financial transparency look like?

CPBB co-founders faced the exact same dilemma when the principles of Fiscal Health were created to address these very issues. The budget book, the certified annual financial report (CAFR), and reports out of the financial system are great tools for finance professionals, but they prove insufficient to clearly and simply answer the question: is the organization in "good shape" or is there trouble on the horizon?

Furthermore, in a world of rapidly changing economic variables, the answer to that question today might not be the answer to that question tomorrow. (A recent ICMA report on this very subject appeared on this blog just recently: fb.me/16mc7uKUg)

First and foremost, local governments must be clear and transparent about what

truly is their picture of fiscal health. Communicating that picture simply and clearly without volumes of numbers, spreadsheets, tables, and an endless series of charts is frankly a challenge that has plagued financial managers for years. If local governments are going to be able to demonstrate financial reality internally to elected officials and staff, and externally to residents, they have to find better ways to make fiscal situations understandable and transparent to everyone.

The key breakthrough in this area has been "data visualization" which allows for the easiest way of creating a common view, a common perspective that is simple and that everybody can agree on. Part of the reason that financial problems can be obscured or hidden is because many times decisions makers have no idea how to understand finances to begin with.

Data Visualization allows us to create a common view of the financial situation that is simple to understand and interpret, describes the clearly defined variables that can impact the financial situation, allows for "live" and "real-time" changes in these variables, and offers the ability for "dynamic" modeling of "what-if" scenarios - this is how transparency is created, and this is the essential first component of the paradigm shift required.

CPBB Web-based Economic Modeling Tool Overview

Shifting the Paradigm Part 2: Resource Allocation through Priority Based Budgeting

The second component of the paradigm shift is changing the way that resource allocation discussions take place. Financial problems are also effectively hidden and obscured because the budget process allows for it. Line item budgeting, incremental budgeting, zero-based budgeting were each attempts to better understand "how" money is spent, but these methods fail to address a more fundamental question: "why" money is spent.

To the point of the Volcker-Ravitch report, the question of whether or not public dollars are being used effectively is not answerable with the tools currently available to elected officials, decision makers, staff and citizens.

Priority Based Budgeting provides a comprehensive review of the entire organization, identifying every program offered, identifying the costs of every program offered, evaluating the relevance of every program offered on the basis of the community's priorities, and ultimately guiding elected and appointed officials to the policy questions they can answer with the information gained from the Priority Based Budgeting process, such as:

What is the local government uniquely qualified to provide, offering the maximum benefit to citizens for the tax dollars they pay?

What is the community truly mandated to provide? What does it cost to fulfill those mandates?

What programs are most appropriate to fund by establishing or increasing user-fees?

What programs are most appropriate for establishing partnerships with other community service providers?

What services might the local government consider “getting out of the business” of providing?

Where are there apparent overlaps and redundancies in a community because several entities are providing similar services?

Where is the local government potentially competing against private businesses within its own community?

Incredibly, just one week ago, as if to accelerate the ushering in of the "New Wave," the credit rating agency Standard & Poor's upgraded the bond rating of Douglas County, Nevada by two levels, from A+ to AA, citing evidence of the County's efforts "to implement several fiscal health practices, including long-range financial forecasting, revenue and expense stabilization, and priority based budgeting."

The New Wave - Over 60 Communities

It is of utmost importance that all local government communities take to heart the warning and recommendations outlined in the Volcker - Ravitch report. Only the most innovative public entities have made strides in changing their structural approach to long-term fiscal health. And with the economy showing some signs of improvement, many will continue to operate as if to preserve the status quo and vainly wish for increased revenue. This approach represents a philosophy of wishful thinking that will only lead to failure.

The "New Wave" represents efficiency and innovation in this Era of Local Government. The new wave represents a golden opportunity for local government communities. Finding creative, clear, and transparent ways to demonstrate what the next 5 to 10 years might look like is a must if local government professionals are going to address fiscal concerns. All too often, local governments are unable to make sound, timely decisions regarding investing in new resources, starting new programs, or initiating major capital projects because elected officials, local government managers, and staff members are paralyzed by the uncertainty of whether they actually have enough money to appropriate for these purposes.

Among the wide range of services available through the

Center for Priority Based Budgeting™:

"Priority Based Budgeting" Process Implementation

Fiscal Health Diagnostic Assessments

"Fiscal Health Diagnostic Tool" Development

Utility Rate Modeling (using our "Fiscal Health Diagnostic Tool")

Facilitated Goal-Setting / Strategic Planning Retreats and Workshops

Citizen Engagement Facilitation

Fiscal Health and Wellness Workshops

Financial Policy Development

Revenue Forecasting Support

Revenue Manual and Program Inventory Development

Capital Improvement Plan (CIP) Development and Prioritization

Performance Measures and Metrics Assessments

Internal Service Fund Analysis and Development

Asset Utilization and Asset Replacement Studies

Program Costing Support (direct, indirect and overhead components)

Bond rating growth strategies

Local government communities must consider a completely different perspective.

In order to achieve success and accept the challenges that are ahead, we

must see more clearly how to manage, use, and optimize resources in a

much different way than has been done in the past. This new environment

demands a new (economic) vision of the future.

Over 60 communities have now embraced the New Wave of Fiscal Health and Wellness through Priority Based Budgeting. Cities and Counties must ask themselves only one question when considering whether they are truly committed to the fiscal health and successful economic future of their communities for the benefit of their citizens.... "To be or not to be."

Keep an eye on the CPBB blog for further updates. Sign-up for our social media pages so you stay connected with TEAM CPBB!

At the Center for Priority Based Budgeting, we've been extremely interested for some time in how

credit rating agencies (CRA's) would evaluate the Priority Based

Budgeting (PBB) efforts of the communities we're working with. Our core concepts of fiscal health and priority based budgeting have proven to ensure that local governments are clear and transparent about what truly is their economic reality. Communicating that picture simply, clearly, and understandably without volumes of numbers, spreadsheets, tables, and an

endless series of charts is frankly a challenge that has plagued

managers for years. If managers are going to be able to demonstrate

financial reality internally to elected officials and staff, and

externally to CRA's and residents, they have to find better ways to make fiscal

situations understandable and transparent to everyone.

Finding

creative, clear, and nontechnical ways to demonstrate what the next five

to 10 years might look like is a must if people are going to address

fiscal concerns. All too often, local governments are unable to make

sound, timely decisions regarding investing in new resources, starting

new programs, or initiating major capital projects because elected

officials, local government managers, and staff members are paralyzed by

the uncertainty of whether they actually have enough money to

appropriate for these purposes. Developing a long-term financial

forecast is key to gaining a better understanding of what the future

might hold.

How CRA's assess municipal bond ratings for a community has a tremendous impact on the communities ability to borrow. A municipal bond is a bond

issued by a local government, or their agencies. Potential issuers of

municipal bonds include states, cities, counties, redevelopment

agencies, special-purpose districts, school districts,

public utility districts, publicly owned airports and seaports, and any

other governmental entity (or group of governments) at or below the

state level. Municipal bonds may be general obligations of the issuer or

secured by specified revenues.

Municipal bonds are securities that are issued for the purpose of

financing the infrastructure needs of the issuing municipality. These

needs vary greatly but can include schools, streets and highways,

bridges, hospitals, public housing, sewer and water systems, power

utilities, and various public projects.

Communities are seeking every possible means to prevent downgrades in their ratings (and simultaneously increase ratings). And the credit rating agencies are facing immense pressure to substantiate the ratings they report - strong or weak. We've been keeping a close eye on this as we better understand how the CRA's perceive how priority based budgeting can provide evidence that a community is taking a sustainable and responsible approach to resource allocation, basing decisions on the long-term health of the community in light of its values and priorities.

And we've seen mounting success in priority based budgeting communities that CRA's

undeniably value the long-term fiscal responsibility that PBB brings to public entities. Our first case study focused on the city of Chesapeake, Virginia. In August 2011, the three major bond rating agencies reconfirmed their prior ratings and each gave the city a "stable outlook." Per the press release, "the rating agencies confirmed the City's strong ratings, based in part on the evidence of their long-term view."

"There

is no question these are difficult times for governments at all

levels," said the city manager. "The Chesapeake City Council has said time and

again that we must keep our focus on our long term goals, while still

maintaining the best quality of life for our citizens. These ratings

provide clear evidence that we are indeed charting a sustainable course

for the City's future."

"The

three ratings are a testament to the conservative and forward-looking

fiscal management leadership of Chesapeake's City Council and staff,"

said the city manager. "Achieving a ‘stable outlook,' given the current economic

challenges facing cities locally and across the nation, speaks volumes

to the hard work our staff and elected officials have done to

strategically position Chesapeake for continued success."

Then, in 2012, Standard and Poor’s rating agency gave Douglas County, Nevada, an A+ bond rating for its “strong and imbedded financial management practices.” Douglas County has been one of the most successful implementers, and now practitioners, of priority based budgeting. In fact, they were the first county in the nation to implement priority based budgeting.

In 2012, the County embarked on the priority based budgeting process with one of the primary objectives being to bring their community into an ownership position with respect to decision making. What unfolded in their ground breaking use of an online tool to engage citizens sets the bar at a whole new level in participatory budgeting (see story here).

Per the Douglas County bond rating press release, "We have made great progress implementing solutions to long-term challenges, including strong financial management, regional partnerships, infrastructure investment and business development," said County Manager Steve Mokrohisky. "Our local economy is still in a slow recovery and we have a lot of work to do to address critical issues such as road maintenance, main street revitilization and duplication of local services, but we are moving in the right direction and there is reason to be optimistic about the future."

Additionally, Douglas County began developing 5-year financial forecasts to address long-range financial challenges, rather than short-term fixes. As a result, the County has been successful in closing the $3 million annual shortfall in its General Fund, through long term contracts with employees, elimination of positions and regional partnerships that stabilize expenses. The County has also implemented a new priority based budgeting program that focuses on continuous improvement of local services and providing the greatest value to taxpayers.

Now, Douglas County has done it again! Through a multi-year effort, the County's bond rating has just recently been upgraded an unprecedented two notches from A+ to AA. Per the press release (below and here), "the rating upgrade is a significant event for the Countyand reflects recent efforts to implement several fiscal health practices, including long-range financial forecasting, revenue and expense stabilization and priority based budgeting."

Congratulations to Douglas County, Nevada, for their masterful stewardship of local government resources, ability to successfully orchestrate a sound short and long-term economic plan, and thus a well-deserved, concrete AA bond rating! Bravo!

PRESS RELEASE

Douglas County’s Bond Rating Upgraded

to Highest in History

January 13, 2014. Minden, Nevada.

Standard

and Poor’s (S&P) Rating Services upgraded Douglas County’s underlying bond

rating by two notches to ‘AA’ or “very strong” on January 10, 2014.The new bond rating is the first upgrade in

10 years and is the highest underlying rating ever provided to Douglas County from

S&P.The rating upgrade is a

significant event for the County and reflects recent efforts to implement

several fiscal health practices, including long-range financial forecasting,

revenue and expense stabilization, and priority based budgeting.

“This historic upgrade is the

result of our unwavering commitment to excellence,” said County Manager Steve

Mokrohisky.“The fact that our rating

was increased by two notches is significant and demonstrates the impact of the

financial practices that we have implemented over the past several years.The leadership of our Board, the tireless

efforts of our staff and the support of our residents is reflected in this upgrade.”

A higher bond rating allows the

County to lower the cost to taxpayers for financing public projects, and is

considered a reflection of an organization’s high quality financial management,

very low credit risk and very strong capacity to meet its financial

commitments.

In its rating upgrade, S&P referenced

the County’s financial management practices that have been implemented over the

past three years, stating, “We view the county’s management conditions as very

strong with strong financial practices that are well embedded, and likely

sustainable.”S&P concluded that,

“The stable outlook reflects Standard and Poor’s opinion that county officials

will likely continue to manage general fund operations prudently, making the

budget adjustments necessary to maintain stable financial operations and very

strong available reserves.Therefore, we

do not expect to change the rating over the two-year outlook horizon.”

S&P also referenced the County’s recent success in

structurally balancing its budget, stating: “Officials balanced the 2014 budget

. . . We believe officials have successfully

implemented corresponding

expenditure adjustments, permitting the county to add to reserves in fiscal

years 2012 and 2013 after consecutive deficits in fiscal years 2009-2011.”

S&P’s bond rating upgrade

comes just six months after Moody’s Investors Services, Inc. rated Douglas

County with its third highest bond rating of ‘Aa2’ in 2013.Standard and Poor’s Rating Services previously

rated Douglas County ‘A+’ or “strong” in 2012.In 2012, S&P stated that the highlights of the County’s management

techniques were its formal financial policies, utilizing external and internal

resources for budget assumptions, and engaging in multiyear financial planning,

but noted that it wanted to see these practices continued before upgrading its

rating.The last upgrade from S&P

was in 2004, when the County’s bond rating increased one grade from ‘A’ to

‘A+’.

In the last several years, bond rating agencies have

created more stringent criteria for local governments to meet in order to

maintain their ratings.Numerous municipal

bankruptcies have been filed since 2010, due to declining revenues, increasing

expenses and unfunded employee benefit liabilities.Visit www.douglascountynv.gov

for additional information.

Most state and local government entities are obligated to assemble and publish an annual financial report (AFR) once a year. Whether the report is in the form of a Federally guided comprehensive annual financial report (CAFR) or a locally guided annual financial report (AFR), these municipal AFR's generally range from 110 to 250 pages, can take up to six months to complete and are intended to identify service provisions and the fiscal position of the organization.

In December 2013, the International City/County Management Association (ICMA), in conjunction with Northern Illinois University's Center for Governmental Studies, published a white paper titled Management's Perceptions of Annual Financial Reporting. This survey sets out to not only describe "the well-known, complex state of public sector financial reporting," but more importantly to "explore management's perspectives on how the various financial statements affect management, provide a benefit to stakeholders and assist management with understanding and implementing changes to their year-end financial statements."

The Center for Priority Based Budgeting (CPBB) is in business to assist local government leaders

who are seeking service excellence, transparency to their stakeholders, a strong desire to achieve long-term fiscal health and to achieve the Results that are important to their

community. This financial survey is of great importance to us as we strongly advocate the importance of using municipal fiscal data in the most innovative and effective ways possible. This includes economic fiscal modeling, multi-year budgeting and providing a "picture of fiscal health" through data visualization (which allows management and elected officials to actually see and model the current and future fiscal economic health of their community).

Key Survey Results

The two key local government consumers and, coincidentally, producers of these reports are:

city/county managers and administrators

finance officers/directors/managers

These two groups are collectively referred to as "management" going forward.

For entities reporting in accordance with generally accepted accounting principles, annual financial reports offer management a comprehensive view of their finances that acknowledges economic events.

These annual financial reports are valuable resources for assessing fiscal conditions, conducting comparisons to comparable entities and integrating their other managerial roles such as capital improvements planning, budgeting, strategic planning, investing, financing, benchmarking, etc.

For the most part (64 percent), management uses little to no audited financial statements to inform their policy decisions; less than 25 percent use their financial reports to inform their policy decisions.

It is estimated that annual financial reporting costs taxpayers approximately $10k to $50k, with some larger communities spending more than $200k.

Management perceives the purpose (or key benefit) of financial statements to be for compliance and accountability, not as useful information for informing decisions.

Key Survey Recommendations

Reassess content, semantics and structure of annual financial reports. More work must be done to determine how detailed the annual financial reports should be and how the information should be defined, standardized, and structured in order to increase its use in management's decision-making. Most respondents feel that these reports are predominantly a tool for compliance. However, there is rich data in these financial statements that could be used for added input in the decision-making process.

Leverage new technologies. New technologies could lend themselves to include rich details about government's finances without all the "noise" to better articulate the meaning of what is being reported based on the audience/consumer of information. For instance, digitized financial information could allow for consolidated reporting to present the big picture but still allow for others such as tax-payers or investors to go more deeply into the data.

CPBB Observations and Recommendations

What an interesting survey! From our perspective, local government entities (for the most part) are obligated to produce some form of annual financial report. Yet after spending up to six months of staff resources and somewhere between $10,000 to $200,000 of financial resources to produce a 100+ page financial report, less than 25% of local government leaders use their financial reports to inform their policy decisions or for input in assessing future operations?

We see a tremendous opportunity here to better utilize and expand the scope and purpose of annual financial reporting so that this critical economic information can be used for forecasting and will directly tie to all significant policy decisions. And we already have the economic data visualization tools to do just that!

The New (Economic) Lens

Taxpayers

are perhaps expecting local government to provide even more support in

meeting their social, physical, environmental, and economic needs,

especially with the declining assistance in these same areas from

federal and/or state sources.

How does local government continue to offer the important, even vital,

services required by communities in a responsive and timely fashion?

How will finance chiefs address significant debt obligations while maintaining enough resources to provide prioritized services?

What

can managers do to successfully navigate these challenging waters so

that their communities become better, stronger, and more relevant than

ever before? Let’s consider a completely different perspective.

In order to achieve success and accept the challenges that are ahead, we

must see more clearly how to manage, use, and optimize resources in a

much different way than has been done in the past. This new environment

demands a new vision of the future.

For managers, resources can

appear to be scarce because of our tightly clenched grasp on some

commonly held assumptions from which they need to break free. Perhaps

there is a different way to see things. A new lens.

Case Study - Wheat Ridge, Colorado

In 2012, Wheat Ridge City Council

included the identification of core services as a top priority goal in

their strategic plan. The City was already operating at a base level of

service due to budget cuts implemented to cope with the nationwide

economic downturn. In addition, the City continued to face a long-term lack of funding

for Capital Improvement Projects (CIP). With no dedicated revenue

stream to fund more than 250 million in infrastructure projects and a

systemic budget shortfall, 2014 would be the final year the City could

fund minimal preventive maintenance projects with a transfer from the

General Fund. The Fiscal Health Model provided a new visual tool to help facilitate budget discussions. The Fiscal Health Model allows staff to develop live scenarios to provide elected officials an instant picture of the financial impacts of their decisions. One of the more powerful traits of this process is how it has equipped Council and staff with information presented in a format that is resulting in new conversations around budget and resource allocation.

The power of the Fiscal Health Model was realized on May 19th, 2012 at the City Council’s annual planning retreat. City Manager Patrick Goff used the model to show Council members how different

scenarios affected the City’s financial situation. Wheat Ridge

has a backlog of more than $250 million in unfunded CIP projects. The

Fiscal Health Model allowed staff to illustrate to Council, not by pointing to numbers in a budget book but by modeling the financial data, that given

the current fiscal situation, “cutting” the budget to solve the problem

was not a viable option. The City needed to identify new dedicated

revenue sources to ensure the success of these projects in the future. One CouncilMember in particular had a very interesting reaction to this new way of looking at budgeting opportunities.

Although he believes there are still ways and areas to find

efficiencies to save money, he now sees and concedes to the fiscal

realities the City faces. He realizes, as we all do, that no amount of

reductions or cuts would ultimately solve the City’s long-term budget

issues related to capital improvements.

Seeking clearer understanding and communication with your elected

officials?

·Elected officials have adopted Fiscal Health as their

preferred means of communicating with staff regarding any decisions brought

before them that potentially might have a fiscal impact – asking staff to “show

us” those impacts using the principles of Fiscal Health as

the primary communication device.

Working through challenging conversations about compensation

with staff or bargaining units?

·Organizations have entered into labor negotiations with their

bargaining units using Fiscal Health as a way to quickly agree on

the assumptions behind the City’s fiscal forecasts, therefore establishing a

basis of trust in the discussion – then modeling the bargaining units’ requests

to demonstrate impacts to the City’s fiscal position.

Weighing various financial related decisions, with complex variables,

and long-term impacts?

·Fiscal Health modeling is a

powerful scenario-planning tool, providing easy to understand visualization of

data. It has even been used to help a Water and Sewer District prioritize

capital projects, understand the ongoing impacts of those projects, and

effectively develop rate increases by better understanding their ongoing and

one-time sources and uses of funding in their operation.

Local governments choosing to implement the concepts of Fiscal Health

as a treatment regimen are making substantial progress because they are doing

the analytical work required to more accurately diagnosis the reasons behind

their fiscal issues and then determining the best treatments that lead to a

viable cure. Once an organization is on the road to being fiscally healthy, it

can then become more financially sustainable by implementing a Fiscal

Wellness regimen centered around the principles of Priority Based

Budgeting.

Watch a video demo of the CPBB Web-Based (Fiscal Health) Economic Modeling Tool below!

Fiscal Transparency

First and foremost, local governments must be clear and transparent about what truly is their picture

of fiscal health. Communicating that picture simply, clearly, and understandably without volumes of numbers, spreadsheets, tables, and an

endless series of charts is frankly a challenge that has plagued

managers for years. If managers are going to be able to demonstrate

financial reality internally to elected officials and staff, and

externally to residents, they have to find better ways to make fiscal

situations understandable and transparent to everyone.

Finding

creative, clear, and nontechnical ways to demonstrate what the next five

to 10 years might look like is a must if people are going to address

fiscal concerns. All too often, local governments are unable to make

sound, timely decisions regarding investing in new resources, starting

new programs, or initiating major capital projects because elected

officials, local government managers, and staff members are paralyzed by

the uncertainty of whether they actually have enough money to

appropriate for these purposes. Developing a long-term financial

forecast is key to gaining a better understanding of what the future

might hold.

Differentiating between one-time and ongoing

revenues and expenditures to clearly understand how finances are

aligned and where they might be out of alignment is a critical element

in eliminating this uncertainty. Managers understand this principle but

rarely make a concerted effort to be deliberate about depicting this

separation in financial forecasts or budget documents. The need for this

separation is understood but without actually “seeing it,” managers may

not be aware of its impact on the ability to manage and maximize

resources. Not clearly separating the picture into these two revenue

categories may obscure some serious looming fiscal problems.

How

many officials, for example, have approved a capital project without

considering the implications of the associated ongoing costs? Newly

constructed public facilities have sat vacant because of a failure to

separately identify and depict the impact of ongoing operational costs.

Adhering

to this philosophy of differentiating between one-time and ongoing

revenues and expenditures also helps ensure that an organization “spends within its means.”

This concept is not just about balancing the budget but allows managers

to be clear that ongoing operational expenses are funded through

ongoing revenue streams. Using such one-time monies as fund balance or

grants to support ongoing operations is an unsustainable practice. “How

much do you need?” Isn’t this the question that leads off most local

government budget discussions? It’s certainly a far easier question to

answer, but shouldn’t the conversation begin with the more difficult and

oftentimes nebulous question of “How much do we have?”

Devoting

more time to revenue analysis is a critical element in gaining a clearer

understanding of 1) what factors truly drive our individual revenue

streams; 2) how to develop more meaningful and accurate multiyear

forecasts, and, most important; 3) how much is actually available to

spend. If managers have more clarity about what factors might impact

revenue sources, they can improve their ability to foresee those changes

before they happen and react to them before they arrive on the

doorstep. By taking a more diagnostic approach, it isn’t terribly

difficult to determine where revenues specifically come from and assess

what internal or external forces might cause them to grow and shrink.

Next Steps

At the Center for Priority Based Budgeting, we're the first to admit we don't have all the answers. However, we do offer unique and innovative concepts and resources that allow local government communities to better understand their fiscal position and comprehensively

model a multi-year variety of financial scenarios that provide options

and solutions based on each individual communities unique goals and

challenges (something very few municipalities perform to their detriment).

"But it's not too late to do something." And that "something," as we've previously stated in this article, is to consider a completely different perspective.

In order to achieve success and accept the challenges that are ahead, we

must see more clearly how to manage, use, and optimize resources in a

much different way than has been done in the past. This new environment

demands a new (economic) vision of the future.

For managers, economic resources can

appear to be scarce because of our tightly clenched grasp on some

commonly held assumptions from which they need to break free. There is a different way to see things!

Keep an eye on the CPBB blog for further updates. Sign-up for our social media pages so you stay connected with TEAM CPBB!

Jon Johnson and Chris Fabian are pleased to share with you that the Center for Priority Based Budgeting officially opened its office on September 1, 2010, with its main objective being to “lead communities to Fiscal Health and Wellness.”

As most of you know, it was our desire from the very beginning of our partnership to create a not-for-profit environment that could support and sustain our work in not only providing advisory services to local governments across the country but also to find ways to continue our research efforts to better understand the fiscal conditions that are impacting local governments from coast to coast. Utilizing a business development technique found in the private sector, the Center was being “incubated” by another successful not-for-profit organization that also serves local governments. Graduating from the incubator in 2013, CPBB is now working with over 60 organizations who have implemented or are currently implementing the processes and tools of Fiscal Health and Priority Based Budgeting.

As before, we are striving to bring the principles of Fiscal Health and Wellness to all communities by teaching, coaching and guiding them in the development and implementation of our unique, creative and proven tools and techniques. We continue to improve upon our “Fiscal Health Diagnostic Tool”, which provides a quick assessment of any organization’s fiscal health status. We also continue to develop our “Resource Allocation Tool” which provides not only a mechanism to set target budgets based on our Priority Based Budgeting approach, but also serves as a way to depict how well any organization is aligning its resources with the programs and services that the community values. Our work has expanded to now include some interesting and successful citizen engagement opportunities with the communities we are partnering with in this work.

We have included our contact information below and hope that we can continue to reach out to those of you we have worked with in the past to further our research efforts as we continually strive to enhance the Priority Based Budgeting process as well as with the concepts of Fiscal Health and Wellness. We also hope to continue the conversation with those of you who have been following our work and share with you the stories of accomplishment and success from the organizations that have implemented Priority Based Budgeting. Please drop us a line anytime – we’re always glad to hear from you. In the meantime, please update your contact information and when you have the chance, check out our blog site to find out what we’ve been doing since our last conversation with you.

- September, 2007: Colorado 10-County Budget Consortium Annual Conference, Breckenridge, CO - "Rx for Fiscal Health - Alignment with Priorities"

- June, 2008: GFOA (Government Finance Officers Association) Annual Conference, Ft. Lauderdale, FL - "Planning for Financial Sustainability"

- July, 2008: National Association of Counties Annual Conference, Kansas City, MO -"Achieving Sustainable Fiscal Health & Wellness"

- August, 2008: ICMA Audio Conference, Golden, CO - "Achieving Fiscal Health: Strategies for Dealing with Fiscal Distress in Today's Economic Downturn"

- August, 2008: Alliance for Innovations Workshop, San Mateo County, CA - "Budgeting for Priorities - Achieving Fiscal Health & Wellness"

- September, 2008: GFOA Training Workshop, Sacramento, CA - "Fiscal First Aid: Achieving Financial Sustainability"

- September, 2008: Kansas GFOA Fall Conference, Overland Park, KS - "Planning for a Sustainable Financial Future"

- September, 2008: Colorado 10-County Budget Consortium Annual Conference, Beaver Creek, CO - "Budgeting for Priorities - Achieving Fiscal Health & Wellness" - October, 2008: GFOA Training Workshop, Providence RI - "Best Practices in Budgeting"

- October, 2008: Alliance for Innovations Workshop, Charlottesville, VA - "Achieving Fiscal Health & Wellness - Budgeting for Priorities"

- December, 2008: ICMA Audio Conference, Golden, CO -"Fiscal Distress: How to Diagnose the Cause and Identify the Right Solutions"

- January, 2009: GFOA Training Workshop, Newport Beach, CA - "Advanced Tools for Finance Officers: Long Term Financial Planning"

- April, 2009: ICMA Workshop, Belton, TX - "Rightsizing to Realities: Achieving Fiscal Health & Wellness (Prioritization)"

- April, 2009: GFOA Training Workshop, Columbus, OH - "Best Practices in Budgeting"

- May, 2009: ICMA Workshop, Monterey, CA - "Rightsizing to Realities: Achieving Fiscal Health & Wellness (Prioritization)"

- May, 2009: ICMA Audio Conference, Washington, DC - "The Promise of Fiscal Health & Wellness (Prioritization)"

- June, 2009: North Carolina Association of CPA's Local Government Conference, Greensboro, NC - "The Promise of Fiscal Health & Wellness (Prioritization)"

- June, 2009: North Carolina Assoc of CPA's Local Government Conference, New Bern, NC - "The Promise of Fiscal Health & Wellness (Prioritization)"

- June, 2009: GFOA Pre-Conference Workshop, Seattle, WA - "Fiscal First Aid: Budgeting Tactics for Bad Economic Times"

- June, 2009: GFOA Annual Conference, Seattle, WA - "The What's, Why's and How's Of Your Government's Fiscal Condition"

- July, 2009: IL-ICMA/IL GFOA Workshop, Naperville, IL - "Rightsizing to Realities: Achieving Fiscal Health & Wellness (Prioritization)"

- July, 2009: GFOA Training Workshop, Denver, CO -"Fiscal First Aid: Achieving Financial Sustainability"

- September, 2009: ICMA Annual Conference, Montreal, Quebec - "Managing Your Budget in Turbulent Times: An In-Dept Review of Fiscal Health & Wellness (Prioritization)"

- February, 2010: ICMA Audio Conference – “Achieving Fiscal Health & Wellness in the NEW NORMAL”

- February, 2010: Virginia Local Government Association (VLGMA) / University of Virginia / Alliance for Innovation, VLGMA Conference, Charlottesville, VA – “The Principles of Fiscal Health & Wellness (Prioritization)”

- April, 2010: Alliance for Innovation Audio Conference – “The Nuts and Bolts of Implementing Fiscal Health & Wellness”

- April, 2010: Presentation to Boulder Tomorrow – “Achieving R.O.I. in Government: How the City of Boulder is Using Priority Based Budgeting to Demonstrate Return on Taxpayer Dollars”

- May, 2010: ICMA Webinar – “Budgeting in the New Normal: Managing Your Budget in Turbulent Times”

- June, 2010: North Carolina Association of CPA's Local Government Conference, Greensboro, NC - "The Promise of Fiscal Health & Wellness (Prioritization)"

- June, 2010: North Carolina Assoc of CPA's Local Government Conference, New Bern, NC - "The Promise of Fiscal Health & Wellness (Prioritization)"

- August, 2010: Virginia Beach, Virginia Workshop – “Implementing Fiscal Health & Wellness”

- October, 2010: GFOA Audio Conference – “GFOA Best Budgeting Practices – Implementing Fiscal Health & Wellness to Achieve Financial Resiliency”

- November, 2010: ICMA Annual Conference, San Jose, CA – “Surviving and Thriving in the New Normal: How Organizations Implementing Fiscal Health & Wellness (Prioritization) Are Surviving These Times”

- January, 2011: GFOA Training Workshop, San Diego, CA – “GFOA Best Budgeting Practices – Implementing Fiscal Health & Wellness to Achieve Long-Term Financial Health and Resiliency”

- January, 2011: GFOA Training Workshop, San Diego, CA – “Tools of Financial Resiliency: Working with Elected Officials; Analyzing Fiscal Health; Engaging Citizens in the Budgeting Process; Implementing Internal Service Funds”

(UPCOMING) March, 2011: ICMA Webinar – “Getting Ready for the Budgeting Process: How to Use Priority Based Budgeting”

(UPCOMING) April, 2011: IL-ICMA/WI-ICMA/Alliance for Innovations Workshop, - “Achieving Fiscal Health & Wellness (Prioritization)"

(UPCOMING) April, 2011: ICMA Webinar – “Getting Ready for the Budgeting Process: Using the Fiscal Health Model to Diagnose and Treat the Causes of Fiscal Distress”

(UPCOMIONG) December, 2011: Colorado Government Finance Officer’s Association (CGFOA) Winter Conference – “Achieving Fiscal Health & Wellness (Prioritization)”